Anticipating Near-Term Structural Change in the Outsourcing Landscape

Can full-service outsourcing to CROs by large biopharma companies sustainably prosecute a clinical development portfolio?

Over the last 25 years, we have seen an ongoing debate among the large and mid-size pharmaceutical organizations about the most effective outsourcing models with contract research organizations (CROs) for their clinical development operations. The two primary models have been full-service outsourcing (FSO) whereby the service provider leverages its people, processes, and systems to conduct trials on behalf of pharma, vs. the functional service provider (FSP) model, whereby the service provider’s staff works mostly within the sponsor’s systems and processes. However, in the last decade we have seen new models arise that are variations and/or a hybrid of FSO and FSP. In late 2022, the Tufts Center for Study Development (TCSDD) and industry leaders worked together to create a new outsourcing model taxonomy (background here) showing the permutations and combinations between FSP and FSO (see Table 1). The sector has evolved to include more selective, custom-fit sourcing models that leverage components of FSO and FSP across the continuum. Table 1 illustrates the key characteristics of FSO and FSP while also describing the variations that have developed between these two primary models.

Table 1. New Taxonomy in Clinical Development Sourcing Models

Source: Getz, K.; Shah, S.; Luithle, J.; Travers, M. Redefining CRO Sourcing Model Terminology to Optimize Outsourcing Strategies. Applied Clinical Trials. Published online September 20, 2022. https://www.appliedclinicaltrialsonline.com/view/redefining-cro-sourcing-model-terminology-to-optimize-outsourcing-strategies.

When FSP started to gain a foothold in clinical research, many traditional CROs were resistant to embracing this new model. Early growth of FSP came mostly from staffing agencies, as the model was more familiar to companies providing staff augmentation using a contractor base. Today, for most top CROs, FSP is a must-have, strategic capability. The early resistance to FSP from CROs was primarily driven out of fear of cannibalizing their full-service business and margin erosion as a result of what they viewed as a “race to the bottom.” But this thinking is flawed because the FSP model utilizes the internal resources previously employed by the customer to do work that is typically outsourced. In actuality, FSP is not cannibalizing the market of work outsourced to a CRO. Rather it is increasing the size of the market by targeting, developing, and growing the scope and scale of functional services within drug development that can be supported via outsourced model.

At the same time, however, we have seen the largest biopharma companies move to the FSP model to both supplement and standardize their “in-house” clinical development operations as a strategic capability advantage. Today, the FSP sourcing model is recognized as the primary approach for the world’s top 10 largest biopharmas, and its prevalence is increasing within the next 10 largest companies when FSP is considered along with its newer, blended variations. This article seeks to address whether the shift to FSP outsourcing reflects a new reality that, among large pharma, the full-service operating model has not fulfilled, as far as the promise of improved speed, consistent quality, and lower costs than if the sponsor kept the work in-house.

This article addresses the following key questions related to the growth of FSP:

- Is this just a pendulum swing or a fundamental shift in large pharma’s approach to clinical development execution?

- Is this shift to FSP a mid- to long-term approach that CROs will need to adopt in order to meet large pharma’s needs and manage margin pressures?

- What can other sectors teach us about unbundling services—the FIPNET vs. FIPCO model?

Pendulum swing vs. paradigm shift

Over the last 15 years, there have been several examples of top 20 biopharma organizations switching their sourcing strategy from sole source provider to multiple providers, or FSO to FSP, and even back again. Cited reasons include reliability of previous model, quality concerns, changes in key leadership, and their comfort with past experiences. So, the natural question becomes is this a swing of the pendulum or will the switch from FSO to FSP continue over time, forcing CROs to continue to have diverse model offerings that will cater to fickle large biopharma sponsors? The answer is this is not likely a swing of the pendulum but, in fact, is a true paradigm shift.

Another way to think about this shift is as an evolution due to market forces, rather than a pendulum swing. CROs first came on the scene in advance of what was expected to be a large patent cliff in the late 1980s and early ’90s. The arrival of CROs led to large pharma customers dialing up their CRO outsourcing while leaving internal teams alone. This reaction helped to solve some, but not all of the problems in clinical development. Hence, in the early 2000s, FSP providers came along to offer necessary variability within pharma’s internal workforce. Diversification of FSP services quickly followed, with offerings growing beyond clinical trial monitoring and data management to include the full spectrum of trial execution as well as patient recruitment and site-directed services such as contracting and payments.

The FSP model also came with a more cost-efficient price point relative to FSO. Additionally, FSP ensured accountability for trial conduct as delivery remained with the customer. Then pharma’s drug portfolios began to accelerate (the Human Genome project helped this), and customers needed quick deployment of project teams, leading to an increase in FSO outsourcing. Now that the need for quick deployment has stabilized, we are once again seeing a shift back toward FSP. The market determines the pendulum swing.

In recent years, large biopharma organizations have come to recognize the core competencies that are needed in-house to drive a strategic advantage in clinical development. Initiatives such as “fit for purpose” and “design for future” have forced the top 20 companies to understand capabilities that need to be in-house to speed development and improve the quality of trial execution.In essence, these “must-have” capabilities beyond trial design include areas such as start-up activities, patient engagement, statistical analysis, and even field forces that cultivate close connections with investigators and data management with a single operating platform providing readily accessible data.

While macro factors may include large pharma, M&As are more focused on bolt-on acquisitions (vs. large consolidations) and the need for one platform to standardize delivery for portfolio prosecution. But the reality is that large pharma’s current M&A strategy is an indictment of the full-service CRO operating model not being reliable in terms of quality, speed, and cost. In essence, large biopharma manufacturers want to be less reliant on their CRO partner’s operating model and believe they can build and sustain a better operating model themselves.Case-in-point, Merck’s in-house clinical development model was recently seen as a competitive advantage for patient accrual over its industry peers, as evidenced in Figure 1 from the British Medical Journal article published in 2022.

. BMJ Open. 2022, 12: e064458, doi: 10.1136/bmjopen-2022-064458")

Figure 1. BMJ: What Drives Cancer Clinical Trial Accrual?

Source: Jenei, K; Haslam, A; Olivier, T; Milijkoc, M; Prasad, V. What Drives Cancer Clinical Trial Accrual?An Empirical Analysis of Studies Leading to FDA Authorization (2015-2020). BMJ Open. 2022, 12: e064458, doi: 10.1136/bmjopen-2022-064458

Since the publication of this article, several of the comparator pharma companies listed in the report have largely switched their sourcing strategy from FSO to FSP, further validating interest in enhancing the in-house” capability to be able to compete. Lastly, the investigator is often the prescriber and, in reality, the customer. In the classic FSO relationship, the connection to the site begins and ends with the trial. In an FSP model, these relationships can have more durability as the focus is on prosecuting the portfolio of clinical trials and not a “one-trick pony.”

Mid- to long-term large pharma sourcing impact for CROs

According to a recent Tufts impact report,1 total spending in the drug development industry on contract clinical services approached $50 billion in 2022 and the top 10 CROs generated $34 billion in clinical services revenue, nearly 70% of spending on contract clinical services.

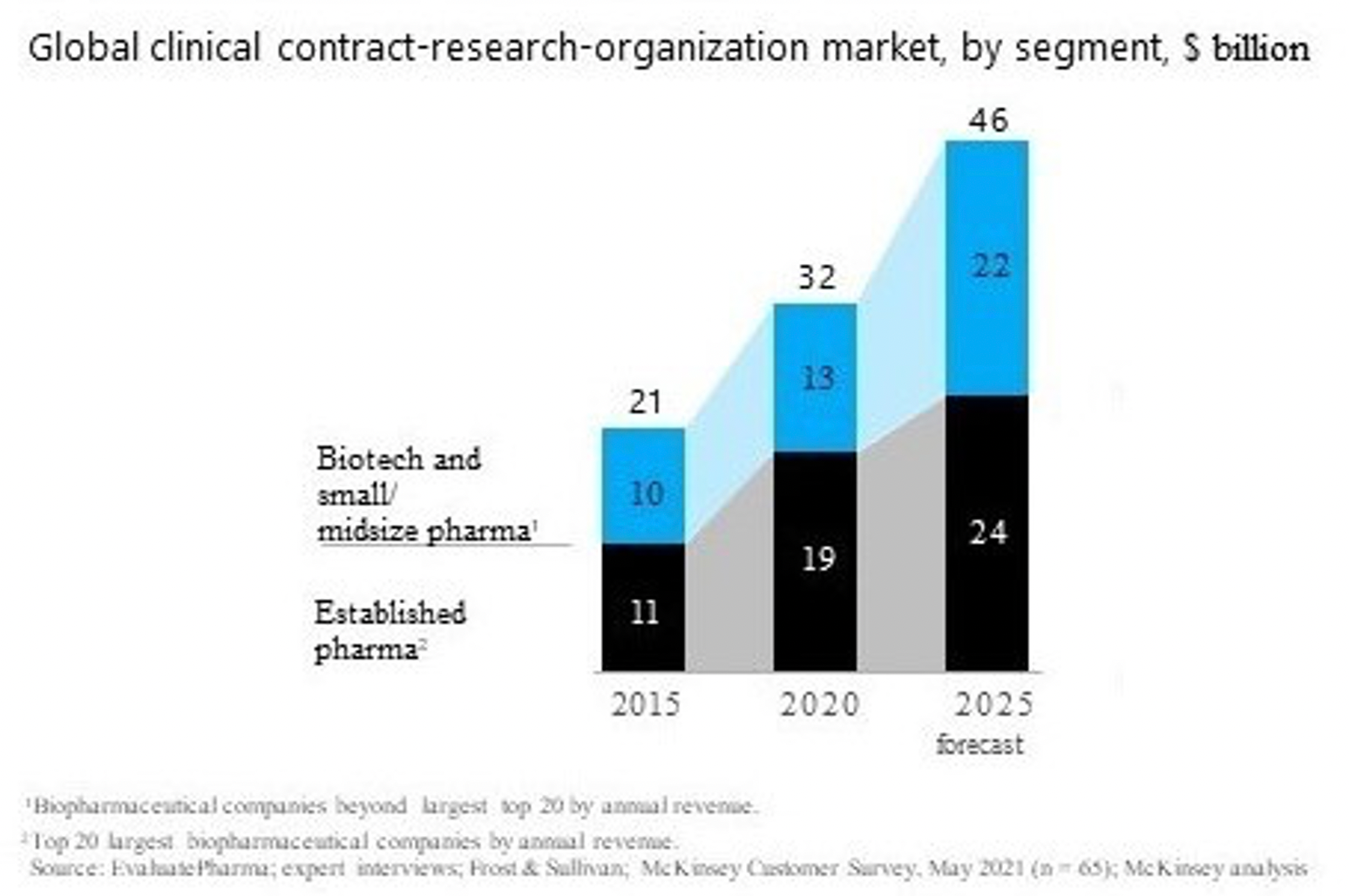

Taking a deeper dive, the clinical outsourcing market, comparing biotech vs. large pharma, is shown in Figure 2. While it is clear that growth will be within biotech/small and mid-size pharma vs. established pharma (i.e., CAGR 2020-25 of 11% vs 5%, respectively), the reality is that, today, established top 20 large pharma still accounts for more than half of clinical outsourcing spend.

Figure 2. McKinsey Report, Survey Results 2021

Source: Bleys, J.; Fleming, E.; Mirman, H.; The, L. CROs and Biotech Companies: Fine-Tuning the Partnership. McKinsey & Company. June 2022. https://www.mckinsey.com/industries/life-sciences/our-insights/cros-and-biotech-companies-fine-tuning-the-partnership#/.

Gross margin expectations for FSP engagements are just under half that of FSO, so the selling, general and administrative (SG&A) pressures will become even more challenging for the top 10 CROs. The impact on CRO balance sheets will be more pronounced by 2025, when most, if not all, of the FSO work for large pharma completes and their backlog is exhausted. By 2025, it is expected that the top 10 largest pharma companies and a majority of the next cohort (11-20) will be in full transition to in-house capabilities that are fully built and operationalized through an FSP sourcing model. So, what does this mean for the large CROs operating at EBIDTA multiples of 9-12x, except for Syneos Health, which went private at an EBITDA multiple of 6.5x? The reality is that SG&A will be under even more pressure, and CROs will need to continue to be nimble in their offerings to large pharma by offering a-la-carte services.

While there may be significant differences in the rates a supplier charges between FSO and FSP resources, the reality is that the direct costs for these resources are essentially the same. Adjusted for experience, the average salary of a clinical research associate (CRA) is not materially different whether they work for a supplier (CRO) or supplier customer (pharma). Additionally, the cost of benefits is comparable, and the incentive structures are equivalent—all characteristic of a mature resource market. This begs the question, why are FSO and FSP rates so different? The answer is that a fully loaded supplier billing rate includes both the direct costs of the resource and overhead allocations (SG&A) as well as supplier margins. If the direct costs are the same, the CROs pricing comes down to the supplier’s ability to leverage its SG&A. These allocated costs include a number of important supporting functions, such as finance, HR, IT, etc. The real challenge is to assign the appropriate level of SG&A within the resourcing model.For a CRO, these include technologies such as clinical trial management system (CTMS), electronic trial master file (eTMF), quality management system (QMS), and learning management system (LMS) tools and supporting infrastructure such as SOPs, training, project delivery, etc. However, large pharma also has these systems and processes in place and requires their FSP suppliers to use them, thus reducing the cost burden for the FSP model to the customer. An FSP rate that is overburdened by these infrastructure costs essentially means that the large pharma customer is subsidizing costs for tools they will not use.

That said, a CRO will likely argue that these systems are required for successful project delivery. This argument, however, misses the primary reason these resources have been outsourced to begin with. Large pharma uses supplier resources to reduce the level of stranded or internal resources and to create a variable workforce model that can ebb and flow with the demands of the development portfolio. If we connect this to R&D productivity, these strategies all relate to reducing the costs of clinical development and/or reducing the cost redundancies of infrastructure that a customer provides and for which the supplier is billing. The supplier who can accurately reflect these required allocations in their bill rates can often deliver the same EBITDA performance as a CRO, even though their FSP rates may be 30% below the typical CRO market rate.

The days when CROs could be selective in offering their “intellect/expertise” only to their full-service customers is myopic thinking at best and will give rise to niche tech and service players, and further dissipate the market to “best-in-class providers.” The reality is that the FSO model will be largely used by biotech and smaller to mid-size (SMID) companies where their clinical capabilities and expertise are not fully built out. However, as large pharma becomes even more sophisticated in its “horizontal purchasing,” the reality of large pharma pricing subsidizing SMID infrastructure will become even more apparent. This, coupled with the pipeline reconfiguration away from large, simplified outcome trials (CV, diabetes, bone fracture, etc.)—trials that require large deployments of resources for a finite period; something a customer would not want to accommodate by hiring a lot of resources)—to smaller trials in precision medicine, cell gene therapy, and rare diseases, further suggests that large biopharma organizations will use less FSO work to prosecute the portfolio outside of: 1) geographic specific needs; and 2) life-cycle studies where risk is relatively low so that internal biopharma company can spend more time on strategic trials.

Learnings from other sectors whereby the horizontal sourcing model prevails: FIPCO vs. FIPNET concept

The emergence of supplier categories in the pharma industry reflects the strategic industry transition from a fully integrated pharmaceutical company (FIPCO) to a fully integrated pharmaceutical network (FIPNET). This transition is not unique to our industry. We have seen examples of horizontal sourcing in the automotive, airline and other large industries. There was a time when Ford owned the rubber plantations that sourced rubber for its tires, and owned the powdered metal facilities that made its automotive parts, etc. However, as the scale of these enterprises grew and other competitors entered the market, these activities were externalized to stand-alone companies (i.e., Firestone tires). It became more economical to work with an integrated network of suppliers than it was to directly own disparate businesses. The same is now true in our industry as there is now a network of providers who can supply best-in-class tools and technologies across the industry. As the scientific and regulatory requirements got more complex, their successful execution requires increasingly specialized vendors. While the large CRO can often serve as a “one-stop shop,” this strategy only works when all stops in the shop are best-in-class. Despite claims to the contrary, it is not clear that any large CRO provides best-in-class offerings across its entire suite of services, and while this may work as a general “contractor” for biotech and SMID, large pharma has now unbundled and purchased best-in-class.

Conclusion

As large biopharma organizations have moved towards developing “in-house” capabilities as a strategic core competency, the CRO service modeling has been forced to adapt to more flexible, a-la-carte offerings and will continue to do so.If the belief holds true that this is not a pendulum switching back and forth between FSO and FSP, but rather, an evolution in the market, then the needs of large biopharma sponsors will need to be heavily considered in investment strategies. While many of the CROs are investing in artificial intelligence (AI), decentralized clinical trial (DCT) platforms, patient consortiums, technology, and real-world evidence as a way to continue to transform their businesses, the application of these innovations needs to be adapted to a service offering that caters to large biopharma companies.This will require careful architecture of systems and processes that can work in a customer’s environment with flexible interfaces, subscription-based pricing, and SaaS working models. For large pharma, contracting with several best-in-breed vendors will allow for innovative advancement of their clinical trials at a portfolio level. Given the unbundling of FSO, a competency in supplier management gives them the ability to work with specialized vendors offering best-in-breed point solutions, from electronic clinical outcomes assessments to trial payments, decentralized or virtual trials, and large and niche players that provide technology and data-enablement offerings across the spectrum of development activities.

Given this shift, large CROs will need to adapt to these new business requirements and regulate their pricing and margin expectations accordingly. This will likely also include ways to monetize assets the CRO has to develop to support clinical trials. Historically, if a customer wanted access to these best-in-class tools, their only option was to hire that CRO to conduct their trials. But these tools are then applied only to that single trial. Large pharma strives for consistency, which means deploying these tools across their portfolio, not just on one or two trials outsourced to a CRO. Bundling these capabilities within a CRO contract also confounds the value proposition, leaving pharma to wonder, are we sourcing to save money or to optimize delivery? The margins for services that either save money or optimize delivery should be different, but CROs often combine them into one pricing model. Thus, the CRO that can assess where and how it creates value for its customers and develops pricing methodologies to reflect this value will have a large advantage in this highly competitive market.

Samir Shah is the Principal of Shah Pharma Consulting Services, LLC. He has more than 25 years of experience in the biopharmaceutical and contract research organization (CRO) industries, most notably pioneering, developing, and maturing a new outsourcing paradigm (functional service provider model) for large and mid-size biopharma companies to prosecute their clinical development portfolios.

Acknowledgement:The author would like to thank and acknowledge the contributions of reviewers David Windley, Managing Director, Healthcare Equity Research, Jeffries LLC; and Ken Getz, Executive Director and Professor, Tufts CSDD.

Reference

- Tufts Center for Study of Drug Development. Impact Report. 4 (6), November/December 2022. https://9468915.fs1.hubspotusercontent-na1.net/hubfs/9468915/NOV-DEC.jpg

")