Reveling in 2018's Revealing Drug and Biologic Approvals

Applied Clinical Trials

Record numbers point to new R&D operating environment, driven by a changing community of sponsors.

Ken Getz

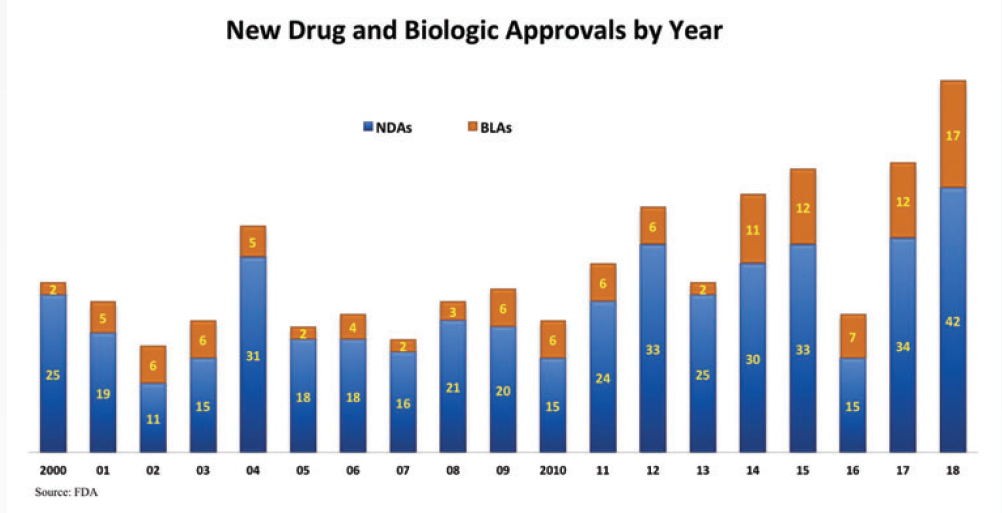

New drugs and biologics approved in 2018 signal an exceptional period of change and opportunity in global drug development. This past year, the FDA approved 59 novel small-molecule (NDAs) and large-molecule biologic (BLAs) therapies-the highest number in history (see chart below).

This is a remarkable achievement, particularly in light of the anemic number of annual approvals that we saw in the 2005 to 2010 period. At that time, several industry watchdogs and prognosticators cautioned that the industry had exhausted its ability to develop truly novel and innovative therapies. They could not have been more wrong.

What is most notable about 2018’s approval volume is not only the scientific innovations that produced them, but also where they originated, how they were funded, and the operating models, services, and technology solutions that supported them throughout the R&D process.

Click to enlarge

Scientific innovation

One revealing feature that sets the 2018 class of approvals apart is the fact that 73% were approved under “priority review” status, meaning they were recognized by the FDA as important, truly novel treatments warranting an accelerated regulatory process. They are therapies targeting medical conditions for which there is no available treatment on the market or they offer substantial improvement over current therapies, including a standard of care.

One-third of all new approvals in 2018 are first-in-class offering a novel mechanism of action-a new way of treating a particular disease. This is another record achieved by last year’s approvals. They represent exciting, truly novel breakthrough therapies, including next-generation vaccines, new antibiotics for drug-resistant infections, combination therapies, nanomedicines, microbiome or bacteria-based treatments, and gene therapies.

Immunotherapies have been one of the leading headliners (e.g., checkpoint inhibitors, CAR-T therapies, and other adoptive cell transfer drugs) and they top the list of breakthrough therapies receiving approval. The first immunotherapy was introduced less than a decade ago; there are now nearly 2,000 cancer immunotherapies in small and large animal studies and in human testing. And immunotherapies that have already been commercialized to treat one form of cancer are now pursuing and receiving regulatory approval to treat many other cancer-related diseases.

In addition to novel therapies, the FDA also approved the use of a record number of already-marketed drugs to treat new disease conditions and to be offered in new formulations that are more effective, accessible, and/or convenient to patients.

Pipeline composition and structure

In addition to notable areas of scientific innovation, new 2018 drug and biologic approvals also reveal a major shift in the composition of the drug pipeline and in the types of companies sponsoring drug development activity. Historically, the majority of new drug approvals targeted increasingly crowded chronic diseases affecting large numbers of people. Nearly 60% of approved drugs today target rare diseases that represent very small markets relative to those for chronic disease-or blockbuster-therapies.

More than one-quarter (27%) of all new approvals are precision medicines. They rely on biomarker and genetic data to identify a far more targeted patient subpopulation that has a much higher likelihood of responding to a new treatment safely and effectively. According to the Tufts Center for the Study of Drug Development (Tufts CSDD), half of all drugs in the overall R&D pipeline-and about 80% of all drugs in development for cancer-related diseases specifically-now rely on biomarker and genetic data to target therapeutic agents.

And whereas new approvals were historically dominated by the largest, top 50 pharmaceutical and biotechnology companies, today the majority of approvals are for drugs in development programs sponsored by small companies-many that are funded by private equity and venture capital. Sixty-percent of new approvals were from sponsors submitting their very first application to the FDA. This, too, is a record achievement.

Small companies have unique needs, including a heavy reliance on outsourcing to support discovery, preclinical, and development activity; a proclivity to seek more open collaboration and data sharing models; and far more limited resources.

Operating innovation on the horizon

In 2018, approximately $150 billion was spent on global R&D activity. Tufts CSDD estimates that R&D spending has been rising 6% annually since 2000. Nearly nine out of 10 drugs entering clinical testing fail, with wide variation in failure rates across different disease conditions. Investigational cancer treatment failure rates are among the highest. Drug development processes are highly complex and inefficient, with durations that have shown little to no improvement in more than three decades. And, on average, the typical drug generates a relatively low and declining return on its development investment, given the high capitalized cost-now estimated at $2.6 billion-to successfully bring a single drug through FDA approval.

To remain viable, drug developers must transform long-standing R&D operating processes and practices that are largely insular and sequential, supported by redundant resources and personnel and that underutilize key assets and expertise. The growing prominence of precision medicines and treatments for rare diseases and targeted patient subpopulations-all requiring more complex clinical trial designs and longer durations to identify and recruit patients-intensify the pressure on drug developers to accelerate this transformation.

Another revealing quality of the graduating 2018 class of NDAs and BLAs is that some are part of an emerging new paradigm that holds promise in delivering better quality, speed, and efficiency at lower cost. According to the Economist Intelligence Unit (EIU), during the past five years, an estimated 3% to 5% of clinical trials were “patient centric,” in that they included patients in clinical trial planning and design and they were executed with approaches that supported greater participation convenience (e.g., use of mobile technologies, transportation assistance, home- and work-based participation). The EIU found that patient-centric clinical trials had Phase II and III enrollment rates that were 40% faster. They also noted that drugs approved with patient-centric clinical trials had higher success rates and a greater likelihood of receiving formulary approval by insurers. Although the numbers are small at this time, we anticipate having more data on approvals in the coming years to further demonstrate the impact of this new operating paradigm.

A growing number of new approvals are also being developed in an environment that favors more open, precompetitive data and information-sharing. New approvals also favor increasing use of external collaborations and service providers that offer scientific and operating expertise and operating advantages, smarter use of resources, and greater leverage of data and analytics to inform, manage, correct, and predict.

During the past several years, we have seen massive investments by traditional R&D players and new entrants, consortia, the capital markets, and the public sector in data and data management capabilities and technology solutions and applications. There is an enormous appetite currently for more sophisticated analytics, including machine learning and natural language processing to analyze a much higher volume of data from diverse sources (including clinical data and real-world evidence such as electronic health and medical records); to prioritize and target resources; to identify and interpret data patterns; to assess and mitigate risk; to manage complex logistical and manufacturing processes; to benchmark practices and, increasingly, to predict scientific and operating outcomes and performance.

Patients and patient advocacy groups are playing a growing role in helping to direct and even fund drug development programs, to define clinically meaningful outcomes, and to push the scientific community to provide higher levels of relevance, convenience, flexibility, and transparency.

We are getting closer to being able to aggregate and look at data across the entire R&D and commercialization continuum. Components of an historically fragmented and disaggregated system within drug development and within the broader healthcare arena are becoming increasingly connected and integrated to share and make better use of scientific and operating data to support open and collaborative learning-what the National Academy of Sciences calls a Learning Health System-where every response a patient has with a commercially-available or investigational therapy informs personalized treatment as well as public health outcomes. As integration unfolds, we expect clinical research and clinical care to converge to drive efficiency through the removal of intermediaries and redundant fixed infrastructure and labor-intensive activity. And we expect patients, payers, and providers to play active roles in the development of new treatments.

We have a long way to go to realize the full promise of this new operating environment and to navigate critical issues like data ownership, data privacy, data compatibility, and the gleaning and refereeing of insights in the data. But, as we revel in 2018’s new drug and biologic approvals, we are already seeing truly novel scientific innovations generated by a changing community of sponsor companies piloting and operating under an evolving drug development paradigm.

There are now more than 11,000 active molecules in the R&D pipeline-a 5-7% year-over-year rate of growth across the span of two decades-to address unmet medical needs and improve patients’ lives. This is indeed an unprecedented moment.

Ken Getz, MBA, is the Director of Sponsored Research at the Tufts CSDD and Chairman of CISCRP, both based in Boston, MA. email: kenneth.getz@tufts.edu